The Master Guide to Investment Accounts

When you start investing, the “what” (stocks, ETFs, bonds) is important, but the “where” (the account type) determines how much of your profit you actually keep versus how much goes to the IRS.

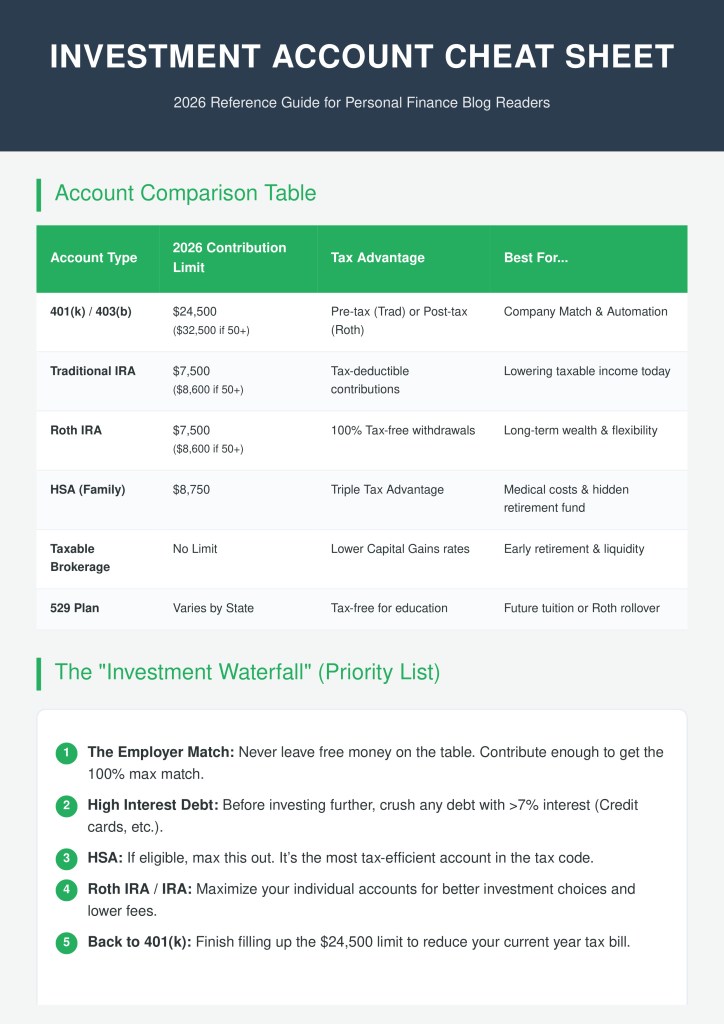

1. Tax-Advantaged Retirement Accounts

These accounts are “wrappers” designed by the government to encourage long-term saving. They come in two main flavors: Traditional and Roth.

Employer-Sponsored Plans (401k, 403b, 457)

- Best for: Automation and getting a company “match” (free money).

- 2026 Limits: You can contribute up to $24,500 ($32,500 if you’re 50+).

- Pro Tip: If your employer offers a match, contribute at least enough to get the full amount. It is an immediate 100% return on your investment.

Individual Retirement Accounts (IRA)

- Best for: Flexibility. You can open these at any brokerage (Vanguard, Fidelity, Schwab) and invest in almost anything.

- 2026 Limits: $7,500 ($8,600 if 50+).

- Traditional vs. Roth:

- Traditional: Tax break today (deductible), but you pay taxes when you withdraw in retirement.

- Roth: No tax break today, but everything (including the growth) is 100% tax-free when you withdraw later.

2. The Taxable Brokerage Account

Think of this as a standard investment account with no “special” tax rules.

- Best for: Flexibility and “Bridge” money (funds you might need before age 59½).

- The Rules: There are no contribution limits and no withdrawal penalties.

- The Cost: You pay taxes on dividends and realized capital gains every year.

- Tax Tip: Hold assets here for at least one year to qualify for Long-Term Capital Gains rates (0%, 15%, or 20%), which are significantly lower than standard income tax rates.

3. The “Secret” Weapons: HSA and 529

The HSA (Health Savings Account)

Many call this the “Triple Tax Advantage” account. It is arguably the best investment vehicle in existence if you have a High Deductible Health Plan (HDHP).

- Tax-deductible contributions.

- Tax-free growth.

- Tax-free withdrawals for medical expenses.

- 2026 Limits: $4,400 for individuals / $8,750 for families.

The 529 College Savings Plan

- Best for: Education savings for kids or yourself.

- 2026 Update: Under recent rules, you can now roll over up to $35,000 of unused 529 funds into a Roth IRA for the beneficiary (subject to annual limits and 15-year account age), making this account much less “risky” if the child doesn’t go to college.

Summary: Which One Should You Use First?

For most investors, the “Waterfall Method” works best:

- 401k Match: Invest enough to get the full employer match.

- HSA: Max this out if you are eligible.

- Roth IRA: Max this out for tax-free growth.

- Back to 401k: Fill up the rest of your $24,500 limit.

- Taxable Brokerage: Use this for any leftover “overflow” money.

Leave a comment